What Do Interest Rate Cuts Mean for Physicians?

- Nisha Mehta, MD

- Sep 20, 2024

- 9 min read

Updated: Feb 21

After a few years of some of the highest interest rates and inflation in the past decade, the Federal Reserve is starting to cut interest rates. Depending on your stage in life, this will have different effects on you as a physician. Those that have a lot of debt like mortgages or student loans that are at higher interest rates may be excited about the idea of refinancing to lower rates and freeing up some room in their monthly budgets, whereas those that were loving their high yield savings account may be disappointed to see rates come down a little bit. If you’re a real estate investor, you’re likely thrilled about the idea of being able to leverage debt to buy more properties. Even if you keep investing simple and invest only in the stock market, the businesses you invest in are deeply influenced by the fed funds rate, so changes in the rate have widespread consequences on the economy as a whole. Below, we’ll explain how the interest rate affects you and how to make decisions based on the cuts.

Disclosure/Disclaimer: This page contains information about our sponsors and/or affiliate links, which support us monetarily at no cost to you, and often provide you with perks, so we hope it's win-win. These should be viewed as introductions rather than formal recommendations. Our content is for generalized educational purposes. While we try to ensure it is accurate and updated, we cannot guarantee it. Rates can change frequently. We are not formal financial, legal, or tax professionals and do not provide individualized advice specific to your situation. You should consult these as appropriate and/or do your own due diligence before making decisions based on this page. To learn more, visit our disclaimers and disclosures.

Article Navigation

What is the federal funds rate, and how does it affect interest rates?

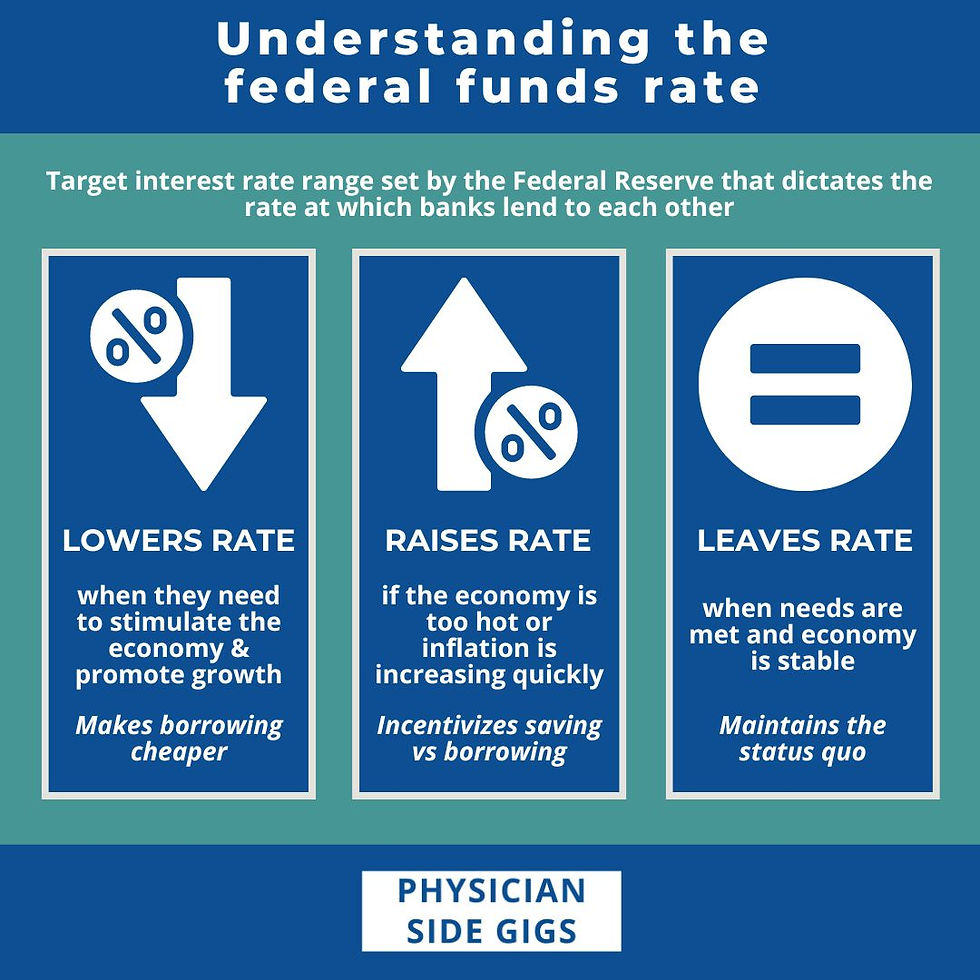

You have definitely heard about interest rates, but you may not have heard of the term “Federal funds rate.” The federal funds rate is the actual target interest rate range set by the Federal Reserve, or more specifically, the Federal Open Market Committee (FOMC) of it, that dictates the rate at which banks (and some other institutions) lend to each other. It essentially sets what these institutions charge each other for short term loans. In case you’re wondering why they’re loaning each other money, banks are required by law to maintain a certain percentage of their deposit balances in an account at a Federal Reserve bank, so they often lend excess money in their reserves to each other.

This rate is a huge deal because it significantly impacts the rest of the economy, as it serves as a benchmark for interest rates elsewhere, including mortgages, student loans, car loans, credit cards, savings accounts, commercial loans, personal loans, and bank loans. This in turn affects the financial and stock markets, corporate investment, foreign exchange rates, and personal and business decisions.

When does the Fed increase and decrease interest rates?

Eight times a year, the Fed meets to discuss what it should be set at, based on what they’re seeing in the economy and how they want to support it by promoting economic growth. On 9/18/2024, the Fed cut the fed funds rate by 50 basis points to a range of 4.75% to 5%. This was the first rate cut in over 4 years because of widespread inflation after the pandemic - you may recall that when the pandemic hit, the Fed had responded dramatically, slashing interest rates to 0.0%-0.25% in an effort to keep money circulating in the economy.

Although this is a somewhat complicated and subjective concept, there are basic principles that dictate increases or decreases in the federal funds rate:

The Fed will generally lower the rate when they need to stimulate the economy and promote economic growth, or to prevent increases in unemployment. What this does is to make borrowing cheaper, which then allows businesses to grow faster and spend more, because they don’t have to worry as much about paying high interest on their debt.

The Fed will generally increase the rate if it’s felt the economy is overly hot or if inflation is increasing too quickly. By making it harder to borrow money, it encourages businesses and people to be better savers and not spend irresponsibly.

The Fed can also elect not to change rates at all when it meets (and often does if things feel stable).

The amount that the Fed chooses to change interest rates by will reflect how urgent the Fed feels it needs to intervene. While most of the time it elects to change the interest rate by 0.25% (or 25 basis points), sometimes it will make larger shifts of 0.5% (50 basis points) or more.

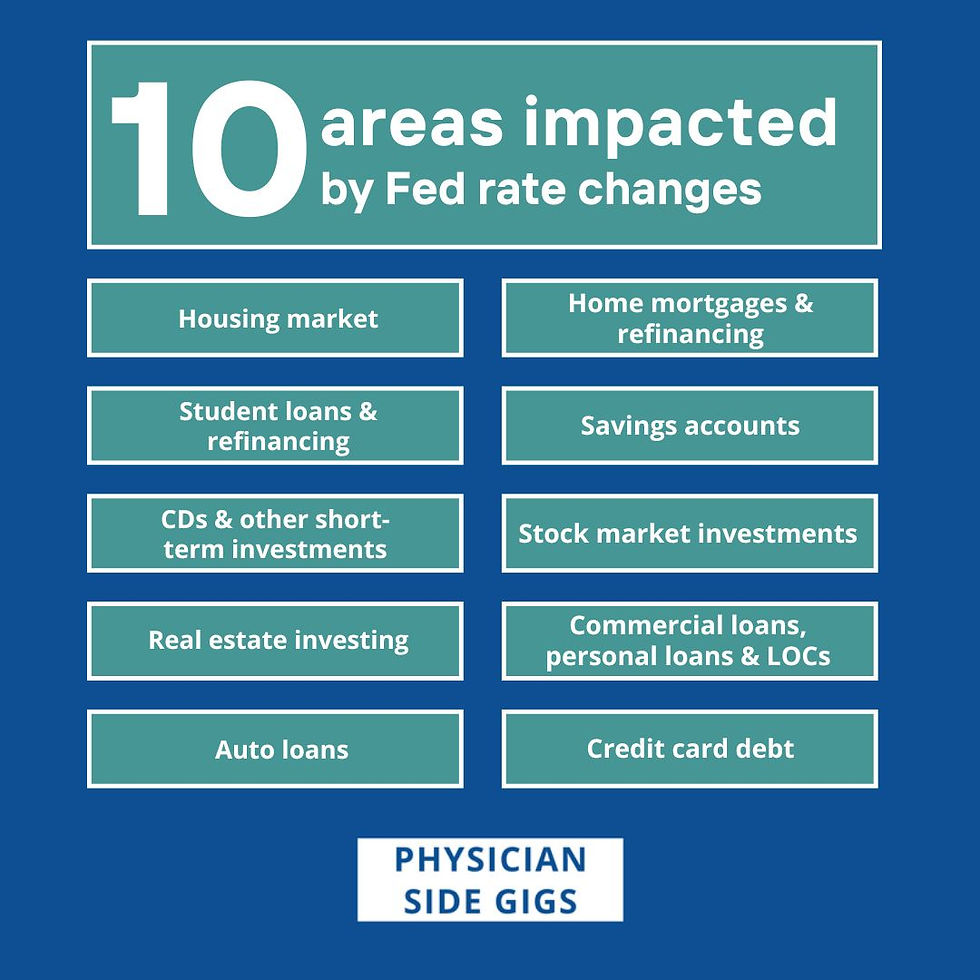

How federal rate cuts and declining interest rates affect doctors

It’s important not to make major decisions off of a single rate cut, but if rates continue to decline, there are some general concepts to keep in mind when thinking about how you manage debt, save, and invest.

Home ownership and mortgages

Over the last few years, we’ve seen physicians looking to buy a new house lamenting about how much harder it is to afford the mortgage because of how much interest is in every monthly payment, as well as how low housing inventory on the market is. Because the size of the mortgage payment affects how much house you can afford, many physicians have had to buy smaller houses than they could have a few years ago, or have deferred on moving or purchasing their first home. As we saw in the week preceding the interest rate drop, if interest rates continue to drop, mortgage rates and the cost of home ownership related to debt should also continue to drop. Eventually, lower mortgage rates will also mean more people are willing to leave their current homes, which will hopefully result in more homes on the market. It’s important to note that while the cost of debt goes down, it doesn’t necessarily mean that home prices will go down, as increased demand or market activity could actually push home prices up depending on the forces within the market.

PSG Perks and Resources:

Contact our recommended mortgage lenders for physicians if you need help with a mortgage.

Contact our recommended real estate agents for physicians if you need help buying a home.

Mortgage refinancing

Similarly, for those physicians who have bought houses in the last year or two, questions about whether you should refinance your mortgage have started to pop up. However, it’s important not to jump at refinancing unless you’re sure it will really work to your benefit. For example, if you’re anticipating a move in the next year or two or if you anticipate paying off your mortgage soon due to a financial windfall, it likely doesn’t make sense to pay the costs of a mortgage refinance.

It’s important to run the numbers with a mortgage lender and see how much interest you are really saving, because unlike student loan refinancing, there are significant costs associated with a mortgage refinance. If further cuts are anticipated in the near future, you may find yourself wanting to wait a little while to refinance your mortgage, as you don’t want to pay mortgage refinance costs every time the interest rate drops a little bit. Learn more about when to refinance your mortage.

PSG Resources and Perks:

Our sponsor, Tom Raschka, NMLS 205578, is a mortgage agent that specializes in assisting physicians with their mortgage refinancing needs. You can contact him here to explore refinancing today.

Brian Smith (bsmith@fairwaymc.com) with Fairway Independent Mortgage has partnered with Physician Side Gigs to offer options for refinancing in 25 states: AL, AZ, AR, CA, CO, FL, GA, ID, IA, KS, MO, MT, NE, NV, NC, OH, OK, OR, SC, SD, TN, TX, VA, WA, and WI. NMLS# 1452834

David Edmondson (david.edmondson@td.com) with TD Bank offers options for refinancing in CT, DE, FL, ME, MD, MA, NH, NJ, NY, NC, PA, RI, SC, VT, VA, & DC. NMLS# 1045001

Student loans

Similarly to mortgages, decreasing interest rates mean student loan refinancing rates should start to trend downwards (in fact, at least one of our recommended companies for student loan refinancing partners reached out to let us know that they’ve cut their rates already in the week of the federal interest rate cut).

PSG Perks and Resources:

Use our recommended physician resources for student loan refinancing, including interest rate discounts and cash back.

Contact our recommended financial advisors for physicians if you need help navigating your student loans.

Savings accounts, including high yield accounts (HYSAs and similar)

For those physicians without a lot of debt and that enjoy keeping a lot of money in cash, the lower interest rates may be disappointing to them. Over the last two years, physician savers have enjoyed higher interest rates in savings accounts, especially high yield savings accounts. With HYSAs being as high as 5-6%, people have gotten used to their emergency funds actually churning out some cash. These interest rates will likely trend downwards.

Because interest rates on these accounts were so high, many doctors defaulted to leaving more money in cash. As rates fall, doctors will likely think more about the differences in return (and tax efficiency) between these accounts and historical returns in the market and other investments, and many predict that investment activity will increase.

PSG Perks and Resources:

Learn more about high yield savings and cash accounts.

Learn more about getting started with investing as a physician.

Certificate of Deposits (CDs) and other short term investments

Short term investments, though not always tax efficient, have become increasingly popular over the past few years with higher interest rates resulting in higher yields on certificates of deposit and similar short term investments. As interest rates fall, expect the returns on CDs to also fall. As with the savings accounts, we suspect more doctors will start to ask where they can get higher returns elsewhere.

PSG Perks and Resources:

Learn more about short term investments.

Contact our recommended financial advisors for physicians if you need help creating a personal financial plan.

Real estate investing

Many physicians who enjoy real estate investing for additional income streams have been frustrated by the higher interest rate environment, as it makes it harder to leverage debt in real estate investments for higher profit margins. It has also resulted in real estate investments that they currently hold being less profitable or even in danger of not cash flowing positively if the real estate holdings held adjustable mortgages where interest rates crept up. As interest and mortgage rates ease, it will be easier to make real estate investments cash flow positively.

PSG Perks and Resources:

Learn more about real estate investing for physicians.

Contact our recommended real estate agents for physicians if you need help finding a commercial real estate agent.

Stock market investments

While this part is less clear, the hope in the long term is that lower interest rates make it easier for businesses to borrow money, hire people, and hopefully grow. This is why you can see large gains in the stock market in the days leading up to and following interest rate cuts by the Fed, especially if the interest rate cut is larger than expected. How this translates to long term gains is more nebulous.

PSG Perks and Resources:

Learn more about getting started with investing as a physician.

Contact our recommended financial advisors for physicians if you need help navigating your personal finance goals.

Commercial loans, personal loans, and lines of credit

Those physicians looking to start a private practice or business may see interest rates on commercial loans start to come down.

Similarly, interest rates on things backed by assets like HELOCs or other lines of credit may start easing.

Personal loan rates may move downward slower, as there is more risk inherent in these products and in general these interest rates are higher. However, for physicians with generally good credit scores, lenders may be willing to be more competitive with interest rates.

PSG Perks and Resources:

Doc2Doc Lending provides physicians with fast access to personal loans. Use our affiliate link for a $100 cash rebate with any newly funded loan, a 0.25% discount if you use auto payment, and your first payment due date held for 30-45 days.

Learn more about when personal loans are a good option for physicians.

For practice loans, visit our recommended private practice resources and perks page.

Auto loans

As with other debt mentioned above, we should start to see interest rates on auto loans fall, which will make cars more affordable.

Credit card debt

This is an exception to the rule for generally falling interest rates and debt. Because these are higher risk products, they tend to have high interest rates that are not as affected by small changes in interest rates. If your credit scores are not good, you remain a risk for these lenders, so you may not see a proportionate fall as quickly. However, for physicians with generally good credit scores that qualify for some more competitive APR cards, you may see some differences.

PSG Perks and Resources:

Learn more about 0% APR credit cards and other credit card options.

Conclusion

When interest rates across industries decline alongside the Fed rate cuts, there are widespread implications for the economy and, on a very tangible level, for physicians and their personal and financial lives. While we don’t think anybody should make any hasty decisions based on one interest rate cut, it is time to start thinking about how a lower interest rate environment than the past few years may impact your personal finance strategy.